Recent Articles

Jun

11

2026

11

2026

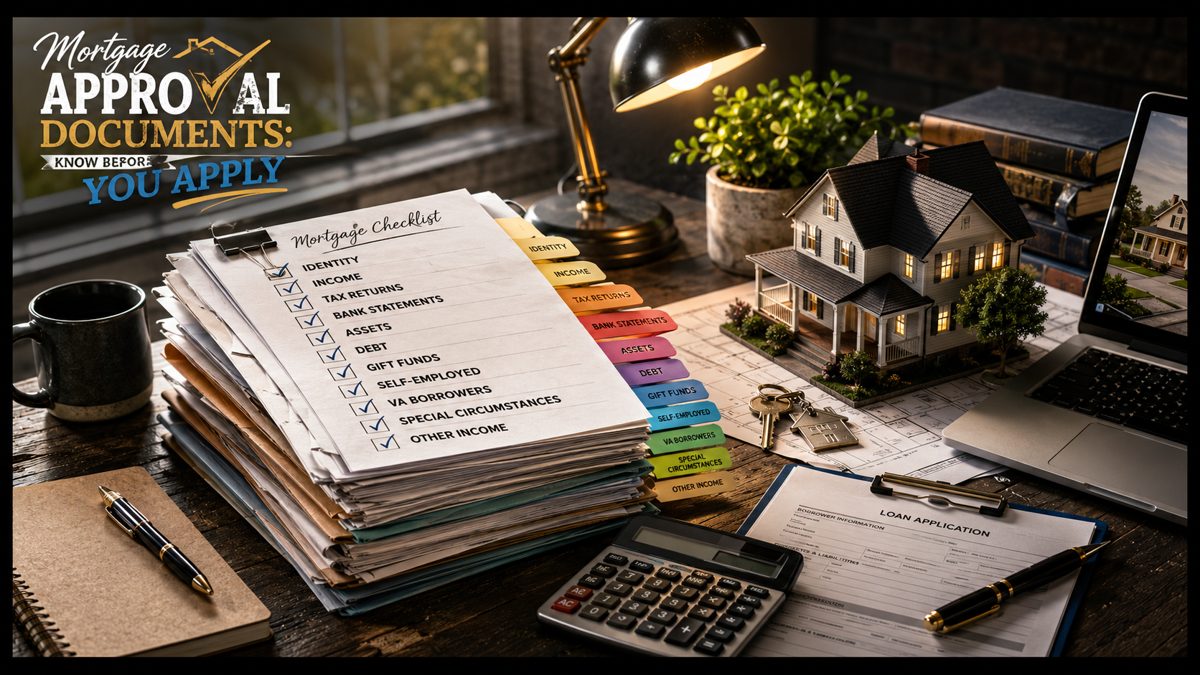

Mortgage Approval Documents: Know Before You Apply

Before you start scrolling through listings and imagining where the couch will go, there is one reality every homebuyer should understand. Finding the house is often the fun part. The real challenge begins when it's time for underwriting. Many home purchase transactions slow down...

Before you start scrolling through listings and imagining where the couch will go, there is one reality every homebuyer should understand. Finding the house is often the fun part. The real challenge begins when it's time for underwriting. Many home purchase transactions slow down...

Jun

01

2026

01

2026

The Wealth Ladder

The Wealth Ladder When people think about building wealth, they often focus on investments, retirement accounts, or growing a business. While those can all play an important role, one of the most common ways families have built long term financial stability is through homeownership...

The Wealth Ladder When people think about building wealth, they often focus on investments, retirement accounts, or growing a business. While those can all play an important role, one of the most common ways families have built long term financial stability is through homeownership...

May

22

2026

22

2026

What If Rates Drop After You Lock?

Locking a mortgage rate can feel like a major decision, especially in a market where rates seem to move constantly. One of the most common concerns homebuyers have is this: What happens if interest rates drop after I lock my loan? The good news is that locking your rate is still one of the...

Locking a mortgage rate can feel like a major decision, especially in a market where rates seem to move constantly. One of the most common concerns homebuyers have is this: What happens if interest rates drop after I lock my loan? The good news is that locking your rate is still one of the...

May

11

2026

11

2026

Mortgage Insurance Has More Than One Face

Most homebuyers hear the term “mortgage insurance” and assume it refers to one simple fee attached to a home loan. In reality, mortgage insurance comes in several different forms, and understanding the differences can save buyers thousands of dollars over the life of a...

Most homebuyers hear the term “mortgage insurance” and assume it refers to one simple fee attached to a home loan. In reality, mortgage insurance comes in several different forms, and understanding the differences can save buyers thousands of dollars over the life of a...

May

04

2026

04

2026

Rate Shopping Mistakes

Most homebuyers assume that collecting more mortgage quotes automatically leads to a better deal. On paper, it sounds logical. More options should mean more savings, right? In reality, rate shopping without a clear strategy often creates confusion, delays decisions, and can even cost...

Most homebuyers assume that collecting more mortgage quotes automatically leads to a better deal. On paper, it sounds logical. More options should mean more savings, right? In reality, rate shopping without a clear strategy often creates confusion, delays decisions, and can even cost...